In a significant and positive reform, the due date for filing Income Tax Returns (ITR) for business and professional taxpayers whose accounts are not subject to audit has been permanently changed from 31st July to 31st August.

This is not a temporary extension — it is a structural amendment in the compliance framework.

What Has Changed?

Earlier:

Non-audit business & professional taxpayers had to file ITR by 31st July.

Now:

The due date is 31st August permanently for this category of taxpayers.

This change applies every year going forward, unless further amended.

Who Is Covered Under This Change?

This revised due date applies to:

✔ Sole proprietors not subject to tax audit ✔ Freelancers and professionals without audit obligation ✔ Small businesses below audit turnover limits ✔ Any business filing ITR where Section 44AB audit is not applicable

Who Is Not Covered?

This change does not apply to:

✖ Taxpayers whose accounts are subject to audit under Section 44AB ✖ Companies requiring audit ✖ LLPs requiring audit ✖ Cases where tax audit report filing date is separately prescribed

Such taxpayers must continue to follow the due dates applicable to audit cases.

Why This Change Is Important

This permanent shift provides:

Better compliance planning

Additional time for finalization of books

Improved reconciliation of GST, TDS, and bank records

Reduced last-minute filing pressure

Earlier, business taxpayers often struggled to close books, reconcile data, and compute taxable income within a short timeline after financial year closure. The additional one month provides practical relief.

Practical Impact

For example:

If a proprietor earns business income and is not liable for audit, their ITR for FY 2025-26 will now be due on:

📌 31st August 2026 (instead of 31st July 2026)

This will continue for future financial years unless amended.

Important Compliance Reminder

Even though the due date is now 31st August:

Advance tax provisions remain unchanged

Interest under Sections 234A, 234B, 234C continues to apply as per law

Late filing fees under Section 234F apply if return is filed after 31st August

Taxpayers should avoid assuming this is an extension — it is the new standard deadline.

Conclusion

The permanent change of ITR due date from 31st July to 31st August for non-audit business and professional taxpayers is a welcome compliance reform. It aligns filing timelines more realistically with business bookkeeping cycles and reduces unnecessary compliance pressure.

If you fall under this category, make sure to plan your filings accordingly and avoid confusion between audit and non-audit due dates.

In a welcome move announced in Budget 2026, the Government of India has simplified the TDS (Tax Deducted at Source) provisions applicable when a resident Indian buys immovable property from a Non-Resident Indian (NRI) seller.

Under the previous system, buyers were required to obtain a TAN (Tax Deduction and Collection Account Number) and deposit TDS using Form 27Q, then file the TDS return separately. This process was more complex than the system applicable for resident-to-resident property purchases.

What’s Changed in Budget 2026?

Starting 01 October 2026, resident buyers purchasing property from NRIs will no longer be required to obtain a separate TAN for TDS compliance. Instead:

✔ The TDS will be deducted and paid using the PAN, just like in resident-to-resident transactions under Form 26QB. ✔ The corresponding TDS return and certificate procedures will mirror the current resident property purchase process. ✔ This aligns NRI seller property transactions with the existing simplified compliance applicable to resident sellers.

How the Current System Works (Until 30 September 2026)

Until the new rule takes effect on 01.10.2026, the current process continues:

The buyer must apply for a TAN.

TDS must be deducted at the applicable rate on the sale consideration paid to the NRI seller.

TDS payment is made using Form 27Q.

A TDS return must be filed quarterly under 27Q.

The NRI seller receives Form 16A as the TDS certificate.

This procedure has been more administratively heavy for resident buyers, especially first-time property purchasers dealing with overseas sellers.

What Will Change From 01.10.2026?

From 01 October 2026 onwards:

✔ No TAN is required for TDS compliance when buying property from an NRI. ✔ TDS deduction and payment will be done using the PAN (similar to resident seller transactions). ✔ The TDS certificate format and return procedures will also follow the resident property purchase model.

Why This Amendment Matters

This reform brings several practical benefits:

Simplified compliance: No separate TAN reduces paperwork and processing time.

Lower compliance cost: No need for TAN registration and maintenance.

Uniformity: The process now mirrors resident-to-resident property transactions.

Ease for residential buyers: Especially beneficial for individual buyers unfamiliar with complex TDS procedures.

Important Notes Before 01.10.2026

Until the new rule becomes effective:

🔹 The existing requirement for TAN and Form 27Q remains valid. 🔹 Buyers must ensure timely TAN registration and correct TDS deposit to avoid notices or interest penalties. 🔹 NRIs receiving the TDS benefit from proper compliance through valid certificates.

Conclusion

The Budget 2026 amendment relating to TDS on property transactions with NRI sellers is a positive step towards simplifying tax compliance for resident buyers. By eliminating the mandatory TAN requirement and aligning the process with existing 26QB systems, taxpayers benefit from reduced regulatory burden and easier compliance.

If you are planning to buy property from an NRI, be mindful of the timeline of applicability — conform to the old process until 30 September 2026, and follow the new simplified route from 01 October 2026.

In recent times, a growing concern has surfaced in the restaurant industry regarding the improper handling of Goods and Services Tax (GST). Some restaurants have been found guilty of canceling their GST registration after a few months but continue to charge GST on their bills. This fraud not only affects the government but also leaves unsuspecting customers at risk of overpaying for their meals.

In this blog post, we’ll explain how this scam works, its impact on consumers, and how you can protect yourself from falling victim to it.

How the GST Scam Works:

Here’s a breakdown of how some restaurants execute this fraudulent activity:

Step 1: Obtaining GST Registration

Initially, the restaurant registers for GST with the government, allowing them to collect GST from customers on food and beverage sales.

Step 2: Cancelling GST Registration

After operating for a few months, usually 6 to 12 months, the restaurant cancels their GST registration with the government. This may be done for a variety of reasons, including to avoid paying the collected tax or simply because they no longer wish to operate under GST.

Step 3: Continued GST Charges

Despite canceling the GST registration, the restaurant continues charging GST to customers. Most customers don’t bother verifying whether the restaurant’s GST registration is still active, which is why the scam works.

Why This Is Fraud:

This practice is a clear violation of the Goods and Services Tax Act and amounts to tax fraud. Here’s why:

Non-Remittance of GST: Restaurants continue collecting GST from customers but fail to remit the collected amount to the government. This means the tax collected by the restaurant never reaches the exchequer.

False Representation: Even after canceling their GST registration, the restaurant continues to represent itself as a GST-compliant business, misleading customers into believing the tax is being handled correctly.

Impact on Consumers:

Overpayment of GST: Customers are unknowingly paying GST on their meals, thinking it is being properly remitted to the government, when in fact it’s not.

Legal Consequences for Restaurants:

Restaurants found guilty of this scam face serious consequences under the GST law:

Penalties: They could be subjected to heavy fines for non-compliance, in addition to penalties for submitting false information to tax authorities.

Criminal Prosecution: Depending on the severity of the fraud, criminal charges may be filed, leading to legal action and even imprisonment for responsible parties.

How to Protect Yourself as a Consumer:

As a consumer, it’s important to be vigilant and take steps to ensure you’re not unknowingly paying GST that isn’t being remitted to the government:

Verify GST Registration: Before paying GST, you can verify whether the restaurant’s GST registration is still active. Visit the GST portal to check their GSTIN status.

Request a Valid Invoice: Ensure the restaurant provides a proper GST invoice with a valid GSTIN. If they don’t provide one, or if the GSTIN is invalid, it’s a red flag.

Report Suspicious Activity: If you suspect a restaurant is involved in this scam, you can report them to the GST department through their official channels.

Conclusion:

The GST scam happening in some restaurants is a serious issue that affects both consumers and the government. By staying informed, consumers can ensure they don’t fall prey to such scams, while businesses that engage in such practices can face severe penalties.

Together, we can help maintain the integrity of the tax system and ensure fair practices in the restaurant industry.

Call to Action:

If you found this article helpful, make sure to share it with your friends and family to raise awareness. For more updates on GST laws and taxation tips, follow our blog.

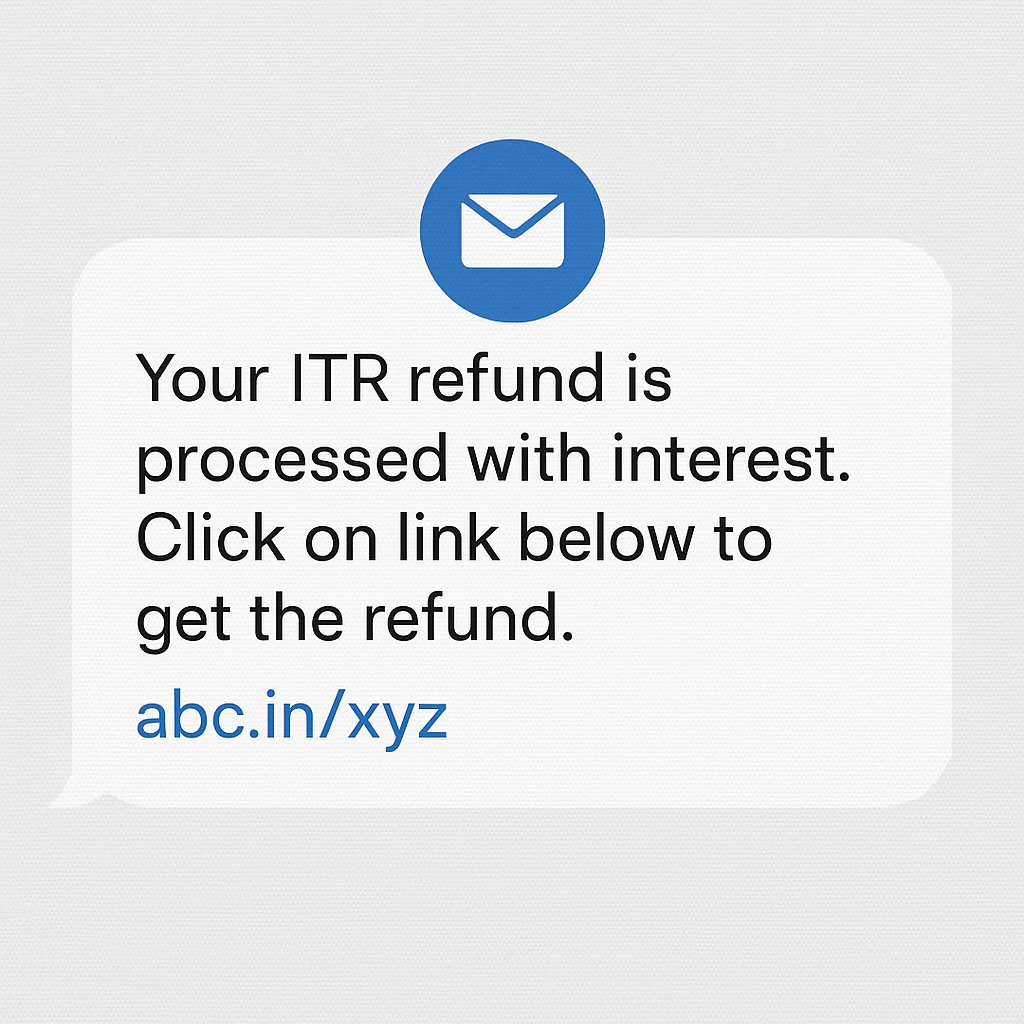

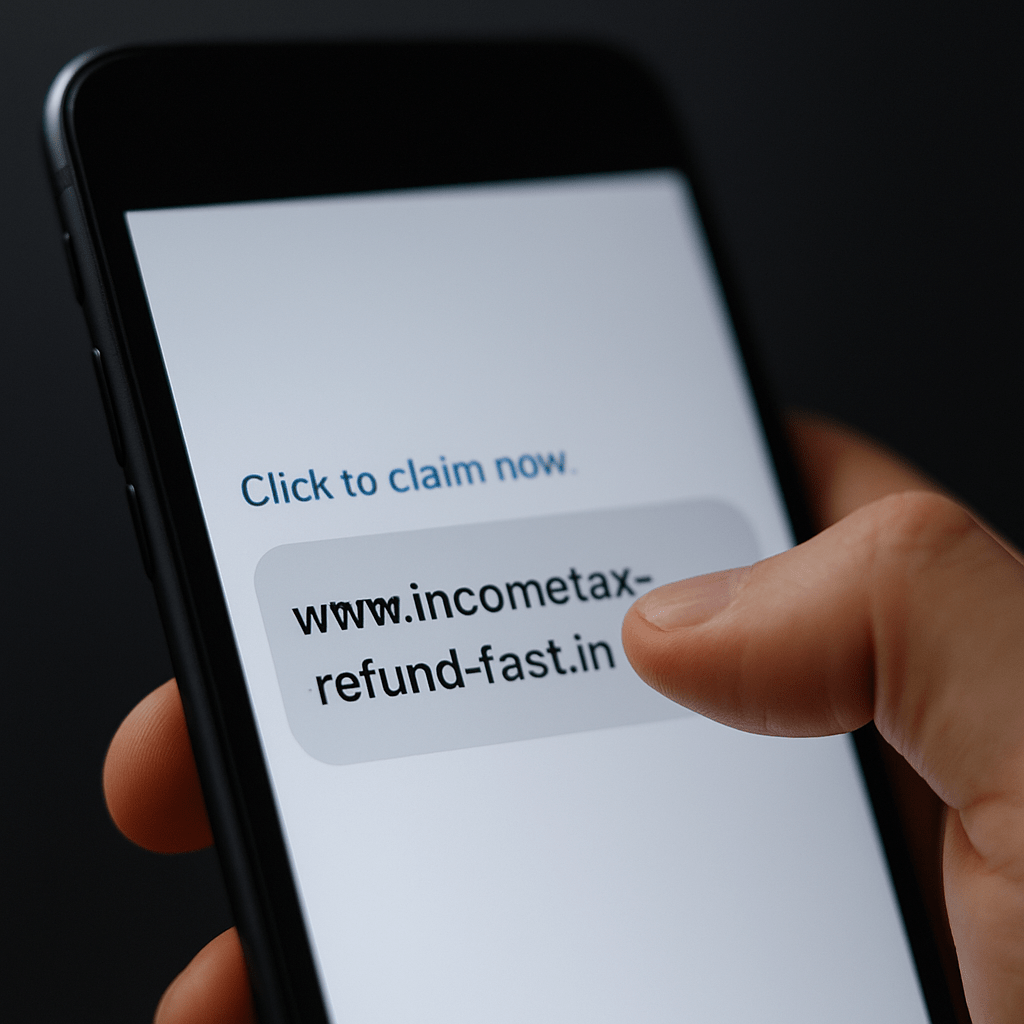

It’s Income Tax Return (ITR) season, and while you’re focused on getting your refunds, scammers are focused on tricking you out of your money. Many people have reported receiving fake messages claiming that their tax refund has been processed with interest — and asking them to click a suspicious link. Here’s what you need to know to stay safe.

⚠️ What Does This Scam Look Like?

Messages claiming your refund is processed with interest

Links mimicking the Income Tax Department site

Requests for bank details, UPI ID, OTPs or card numbers

⚠️ Scam SMS Example:

“Your ITR refund of ₹10,350 is approved. Click here to receive – incometax-refund.in/go/secure”

Looks legit, right? But it’s completely fake.

Most of us feel safe parking our money in a savings account. It’s accessible, feels secure, and seems like a smart default option. But in 2025, this habit may be quietly destroying your wealth.

Here’s why relying on a savings account alone could be one of your worst financial decisions — and where you should actually be putting your money instead.

📉 The Harsh Truth: Savings Account Returns Are Too Low

Today, most savings accounts offer just 2.5% to 4% annual interest. Sounds okay? Think again.

After tax, the effective return can fall below 3%. Meanwhile, India’s average inflation hovers around 5–6%, meaning your money loses value every year.

Example:

₹1,00,000 kept in savings at 3% = ₹3,000/year

Inflation at 6% = ₹6,000 loss in buying power

Net loss = ₹3,000 in real terms

You’re not growing your money — you’re slowly shrinking it.

⚠️ Why This Is Financially Dangerous

Leaving large amounts idle in a savings account creates:

Opportunity loss — you miss better returns elsewhere

No compounding benefits

False sense of “saving” while inflation eats into it

Savings accounts are best used only for:

Emergency funds (3–6 months of expenses)

Daily or short-term transactions

✅ What You Should Do Instead

Here are safer and smarter places to park your money for higher returns:

1. SIPs in Mutual Funds

Start as low as ₹500/month

Historical CAGR: 10–12%

Ideal for long-term wealth creation

2. Fixed Deposits (FDs)

Safer than stocks

Returns: 6–7%

Best for short- to medium-term goals

3. Blue Chip Stocks / Index Funds

Higher potential returns (but market-linked risk)

Best if held for 5–10+ years

Can be started via direct investing or ETF platforms

📊 Smart Allocation Formula

Emergency Fund: 3–6 months of expenses → Keep in savings account

Short-Term Goals: 1–3 years → Invest in FDs or liquid mutual funds

Long-Term Goals: 3+ years → Go for SIPs, index funds, or blue chip stocks

Let your money work for you — not sit idle and depreciate.

🧾 Conclusion: Time to Move Beyond the Savings Account

Savings accounts are not designed for wealth growth — only for liquidity. In 2025, keeping large amounts in them is like putting your money to sleep while inflation eats away at it.

Take control of your finances. Make smart investments. Even small, consistent steps today can lead to massive gains tomorrow.

📣 Ready to Start Smarter With Your Money?

And if you want personalized help with tax-saving investments, planning SIPs, or portfolio setup: 📩 [Contact Us] or 📞 Book a free consultation today!

Introduction: As the 2025 financial year progresses, NRIs (Non-Resident Indians) must pay close attention to the latest tax-saving opportunities. Whether you’re earning in India or abroad, optimizing your tax strategy can save you lakhs. In this blog, we’ll walk you through smart, legal, and practical ways to reduce your tax burden as an NRI.

1. Understand Your Residential Status

Before diving into deductions, confirm your residential status under Indian tax laws. If you qualify as an NRI for FY 2024–25, only income earned or received in India is taxable.

2. Claim Deductions Under Section 80C

NRIs can claim deductions up to ₹1.5 lakh under Section 80C for:

Life insurance premiums

ELSS (Equity Linked Saving Schemes)

Principal repayment of home loan

ULIPs

Tuition fees for children

🔸 Note: PPF and NSC investments are not allowed after becoming an NRI.

3. Section 80D: Health Insurance

Premiums paid for health insurance qualify for deduction:

₹25,000 for self & family

Additional ₹25,000 (₹50,000 if parents are senior citizens)

4. Interest from NRE & FCNR Accounts

Interest on NRE accounts is tax-free in India.

Interest on FCNR accounts (foreign currency term deposits) is also tax-free. These are ideal options for NRIs to park funds from abroad.

5. Avoid Double Taxation Using DTAA

NRIs can use Double Taxation Avoidance Agreements (DTAA) to avoid paying tax twice. You can claim:

Foreign Tax Credit (FTC) on income taxed abroad

Use Form 67 to file FTC before or with your ITR

📌 Ensure you get a Tax Residency Certificate (TRC) and fill Form 10F as required.

6. Save Taxes on Home Loans

NRIs can claim:

Up to ₹2 lakh on interest under Section 24(b)

Principal repayment under Section 80C Real estate investments in India offer both asset growth and tax benefits.

7. Capital Gains Planning

If you sell property or shares in India, plan to:

Reinvest in residential property (Section 54, 54F)

Invest in 54EC capital gain bonds (NHAI/REC) to save tax

8. Section 80E: Education Loan

NRIs can claim 100% deduction on interest paid on education loans (for self, children, spouse) for up to 8 years.

9. Section 80CCD(1B): National Pension Scheme (NPS)

You can get an additional ₹50,000 deduction by investing in NPS — over and above the 80C limit.

10. Section 80TTA: Savings Account Interest

NRIs can claim up to ₹10,000 deduction on interest earned from savings accounts held in Indian banks (NRO).

11. Other Smart Deductions

Donations to eligible institutions (80G)

Premium for ULIPs

Filing your ITR on time — even if income is below threshold — to claim refunds or carry forward losses.

Conclusion: Tax planning for NRIs in 2025 doesn’t have to be complicated. With the right mix of deductions, exemptions, and international tax rules, you can reduce your tax burden and grow your wealth efficiently. Need personalized help? [Contact us] today for NRI-focused tax advisory services.

For Non-Resident Indians (NRIs), navigating tax laws across multiple countries can be complex—especially when income is earned in more than one country. One major concern is double taxation, where the same income is taxed both in India and your country of residence. This is where Double Taxation Avoidance Agreements (DTAAs) come into play.

In this blog, we’ll break down what DTAA is, how it works, and what NRIs need to know to avoid paying more tax than necessary.

🔍 What is DTAA?

DTAA is a treaty signed between two countries to avoid taxing the same income twice. India has DTAA agreements with over 90 countries, including the USA, UK, UAE, Canada, Australia, and Singapore.

🧾 Why is DTAA Important for NRIs?

As an NRI, you may:

Earn salary or business income abroad

Earn interest, dividends, or rental income from India

Be taxed in both countries for the same income

Without DTAA, you could end up paying tax twice on the same income. DTAA helps you:

Lower your overall tax burden

Claim relief via exemption or credit method

Avoid legal disputes or penalties

📘 How DTAA Works: Methods of Relief

There are two main methods under DTAA:

1. Exemption Method

The income is taxed only in one country and exempted in the other.

Example: If the treaty says rental income is taxable only in India, you don’t pay tax on it again abroad.

2. Credit Method

Income is taxed in both countries, but you get a credit in your resident country for tax paid in India.

Example: You paid ₹10,000 tax in India on interest income. You can claim ₹10,000 credit in your resident country to reduce your tax there.

🌍 Common Income Types Covered Under DTAA

Most DTAA treaties cover:

Salary

Interest

Dividends

Royalties

Capital gains

Rent from property

India usually taxes income at source (TDS), and DTAA defines the TDS rate and refund eligibility.

📑 How to Claim DTAA Benefits as an NRI

To claim DTAA relief in India, follow these steps:

Obtain a Tax Residency Certificate (TRC) from your resident country.

Submit Form 10F to the Indian payer or online.

Provide a self-declaration about DTAA eligibility.

Mention relevant treaty articles when claiming tax relief.

💡 Tip: Ensure your TRC includes your name, status, nationality, and residency period.

⚠️ Things to Keep in Mind

Each DTAA has different terms—check your country’s treaty with India.

Not all income may be exempted.

DTAA doesn’t mean you skip filing returns—you still need to comply with Indian tax laws if applicable.

✅ Conclusion

DTAAs are valuable tools for NRIs to avoid paying double taxes and stay compliant globally. However, the technicalities can be confusing, especially with multiple income sources. For smart NRI tax planning and DTAA claims, professional guidance is always a good idea.

📞 Need Help with DTAA Filing or NRI Tax Planning?

Feel free to contact us. At M S Rajpurohit & Co., we specialize in NRI taxation—ensuring you never overpay on taxes.

Disclaimer:

This blog post is for informational purposes only and does not constitute legal or tax advice. Readers are advised to consult a qualified tax professional for personalized guidance based on their individual circumstances. M S Rajpurohit & Co. disclaims any liability for decisions made based on this information.

If you’re a Non-Resident Indian (NRI) with financial ties to India, understanding your tax responsibilities is crucial — especially with frequent updates to tax rules. This guide simplifies NRI taxation in India for FY 2024–25 (AY 2025–26) and helps you stay compliant with Indian Income Tax laws.

Who is Considered an NRI?

As per Indian tax law, your residential status is based on your physical presence in India during a financial year. You are classified as an NRI if:

You were in India less than 182 days during FY 2024–25, and

You were not in India for 365 days or more in the last 4 years + 60 days in the current year

Exception for point (2)

In the case of an Indian citizen or a person of Indian origin (PIO) whose total income, other than income from foreign sources:

Exceeds Rs. 15 lakhs during the relevant financial year – 60 days, as mentioned in point (2) above will get substituted with 120 days.

Indian citizen leaving India for employment outside – The Indian citizen who leaves India in any year as a crew member or for employment outside India, the period of 60 days in point (2) above will be substituted with 182 days.

Hence, an Indian citizen or PIO earning a total income over Rs 15 lakhs (other than from foreign sources) is deemed a resident in India if they are not taxed in any other country.

What Income is Taxable in India for NRIs?

As an NRI, only income earned or received in India is taxable here. Income earned abroad is not taxed in India.

Taxable Income Sources:

Interest on NRO account (taxed at 30% TDS)

Rental income from Indian property

Capital gains from shares, mutual funds, or real estate

Dividends from Indian companies

Income from business/profession (if it arises in India)

Not Taxable in India:

Salary received abroad

Income from foreign investments

Interest on NRE and FCNR accounts (exempt if conditions are met)

When Should NRIs File Income Tax Returns?

You must file ITR in India if:

Your total Indian income exceeds ₹2.5 lakhs

You want to claim a TDS refund (e.g., on property sale or NRO interest)

You wish to carry forward capital losses

Income Tax Return Due Date:

🗓 July 31, 2025 (for individuals not subject to audit). Currently, it is extended to September 15, 2025.

Which ITR Form Should NRIs Use?

Use ITR-2 if you have income from capital gains, rental property, etc.

Use ITR-3 only if you have income from business/profession in India

❌ Do not use ITR-1 (Sahaj) — it’s only for resident individuals.

TDS Rules for NRIs

NRIs face higher TDS rates on certain incomes. Here’s a quick look:

Nature of Income

TDS Rate

Interest/Dividend from investments made by an NRI

20%

Long-Term Capital Gains (LTCG) on: • Shares of an Indian Company • Debentures & Deposits of a Public Co. • Government Securities (as per Sec 115E)

12.5%

LTCG from listed shares & securities under Sec 112A

12.5% (Transfers on or after 23/07/2024 ) 10% (on transfers before 23/07/2024)

Other Long-Term Capital Gains

12.5%

STCG from FII or specified fund (excluding UTI/MF)

20%

Interest on money borrowed in foreign currency (by Govt./Indian co.)

20%

Royalty or technical service fees from Indian concern/Govt.

20%

Winnings from lotteries, games, horse races, online games

30%

Any other income

30%

💡 Note: Applicable surcharge and health & education cess are added over and above these rates.

💡 You can apply for a lower TDS certificate under Section 197 to reduce excess deduction at source.

Tax Deductions Available to NRIs

NRIs are eligible for many deductions available to residents:

✅ Eligible Sections:

Section 80C – Life insurance premiums, ELSS, PPF (till you become NRI)

Section 80D – Health insurance premiums

Section 80E – Interest on education loans

Section 80G – Donations to eligible trusts or funds

❌ Not Eligible:

Section 80TTB – Not applicable for NRIs (this is for resident senior citizens)

Post Office schemes like NSC, SCSS, etc.

Double Taxation Avoidance Agreement (DTAA)

India has signed DTAA with over 90 countries to ensure you don’t pay tax twice on the same income.

To claim DTAA benefits, submit:

Form 10F

Tax Residency Certificate (TRC) from your resident country

Self-declaration of beneficial ownership

DTAA benefits are especially useful for interest, dividends, and capital gains earned in India.

Key Compliance Tips for NRIs

Here are some must-follow tips to stay tax-compliant in India as an NRI:

✅ Apply DTAA provisions if eligible to avoid double taxation

✅ Review and determine your residential status annually

✅ Use the correct ITR form

✅ File ITR even if no tax is due (to claim TDS refund)

✅ Disclose Indian income and foreign assets (if applicable)

Conclusion

NRI taxation in India may seem overwhelming at first, but with the right guidance, it can be managed smoothly. Keep track of your income sources, file your returns timely, and use the benefits offered under law to reduce your tax burden.

📞 Need assistance with NRI tax filing, DTAA application, or TDS refunds? Contact usfor expert help.

About the Author

👤 CA M S Rajpurohit Chartered Accountant | Founder, M S Rajpurohit & Co.

With over a decade of experience in Indian taxation, CA M S Rajpurohit specializes in NRI taxation, and advisory. He’s passionate about simplifying complex tax laws for global Indians and helping clients make informed financial decisions.

The Income Tax Return (ITR) filing season is officially underway. You might feel the urge to file your return as soon as possible—maybe to get your refund faster or just to tick off this yearly chore. But hold on! Filing your ITR too early without waiting for important financial statements could cause you more trouble than you think.

What Are AIS and TIS — And Why Do They Matter?

Before you hit “submit” on your ITR, it’s critical to understand two key documents: the Annual Information Statement (AIS) and the Taxpayer Information Summary (TIS).

Annual Information Statement (AIS): This is a detailed record provided by the Income Tax Department, showing all your financial transactions reported by various entities—banks, mutual funds, employers, and more.

Taxpayer Information Summary (TIS): Think of this as a simplified summary of your AIS, designed to give you a clearer snapshot of your income and tax details.

Both AIS and TIS are essential because they consolidate your financial data from multiple sources and help you file an accurate ITR.

Why You Should Wait for AIS and TIS Before Filing

The problem is, these statements aren’t immediately available when ITR filing opens. The Income Tax Department usually releases AIS and TIS after collecting data from various entities, and this process can take time. Sometimes, the statements are updated and revised multiple times before becoming complete and accurate—often only after mid-June.

If you file your ITR before AIS and TIS are fully updated, your return may miss out on important income details like:

Interest earned on fixed deposits

Dividend income

Capital gains from selling stocks or property

Foreign remittances or credit card transactions reported to tax authorities

Missing these can cause your ITR to not match the department’s data, triggering notices or tax demands later.

Common Mistakes Caused by Early Filing

Here are some common errors taxpayers make when filing ITR too soon:

Forgetting to declare FD interest, which banks report late

Overlooking dividends or mutual fund earnings

Missing capital gains because updated sale or purchase details weren’t included yet

Not reporting overseas transactions or expenses flagged in AIS

These mismatches often invite notice from the Income Tax Department, asking for explanations or corrections—causing stress and extra work.

When Should You File Your ITR?

To avoid trouble, the best practice is to:

Wait until AIS and TIS are fully available and updated, generally post mid-June

Cross-check your Form 26AS (tax credit statement) with AIS and TIS

Reconcile any differences before filing

If you’re unsure or your financial transactions are complex, it’s a good idea to consult a tax expert who can help you analyze these statements and file your ITR correctly.

Final Thoughts

The temptation to file your ITR quickly is understandable, but rushing could lead to costly mistakes and unwanted notices. Take your time, review your financial information carefully, and file only when you’re sure your income data matches the government’s records.

If you need expert help to review your AIS/TIS and prepare your ITR accurately, feel free to reach out. Filing your taxes right the first time saves you headaches later! Contact us.

Frequently Asked Questions (FAQs)

Q1: Can I file my ITR before AIS and TIS are available? A: While you technically can, it’s not advisable. Filing without the updated AIS and TIS can lead to mismatches in reported income, resulting in notices or tax demands later.

Q2: When will AIS and TIS be fully available for filing ITR 2025? A: AIS and TIS are usually updated and finalized after mid-June each year. It’s best to wait until these are complete before filing your return.

Q3: What should I do if I’ve already filed my ITR and then receive a notice from the Income Tax Department? A: Don’t panic. Review the notice carefully, check the discrepancies mentioned, and consider filing a revised return or responding with the correct information. Consulting a tax professional can be very helpful.

Disclaimer

This blog is for informational purposes only and does not constitute professional tax advice. Tax laws and procedures may change. Please consult a qualified tax professional or the Income Tax Department for advice tailored to your specific situation.

Freelancing gives you freedom, but it also brings the responsibility of managing your taxes. From quarterly advance taxes to GST confusion, many freelancers fall into avoidable traps. In this post, let’s look at 5 common tax mistakes and how you can stay compliant (and stress-free).

1. Ignoring Advance Tax Payments

Many freelancers aren’t aware that they need to pay taxes in advance every quarter, not just at the end of the financial year. If your tax liability exceeds ₹10,000 in a year, advance tax payments are mandatory.

Tip: Set reminders for the 15th of June, September, December, and March to avoid penalties.

2. Not Keeping Clear Records of Income and Expenses

Accurate record-keeping is vital for smooth tax filing and to claim deductions properly. Many freelancers mix personal and business expenses or don’t track their income systematically, which leads to confusion and missed tax-saving opportunities.

Tip: Maintain separate bank accounts if possible and use simple accounting tools or Excel sheets to record every payment and expense related to your freelancing work.

3. Overlooking Business Expense Deductions

Freelancers often miss claiming legitimate business expenses like internet bills, software subscriptions, laptops, travel, and home office costs.

Tip: Keep monthly logs and digital copies of all receipts and invoices. This reduces taxable income and maximizes savings.

4. Not Registering for GST When Required

GST registration is mandatory once your annual turnover crosses the ₹20 lakh threshold (₹10 lakh for some states). Many freelancers either don’t know this or delay registration, resulting in penalties and compliance issues.

Tip: Track your turnover regularly. If you’re close to the threshold, apply for GST registration timely manner to avoid trouble.

5. Confusing GST with Income Tax

GST returns and Income Tax Returns (ITR) are separate obligations. Some freelancers assume that filing one means they’re compliant with both, which is incorrect.

Tip: File your GST returns (monthly or quarterly) as per the schedule and also file your annual Income Tax Return accurately to avoid penalties.

Conclusion

Tax compliance may seem complex, but with the right knowledge and habits, you can avoid costly mistakes. Stay organized, set reminders, and consult a tax expert when in doubt. If you want to focus on your freelancing, leave tax worries to us. We are here to help you navigate GST, income tax, and compliance smoothly. Contact Us.